TOP CATEGORY: Chemicals & Materials | Life Sciences | Banking & Finance | ICT Media

Download Report PDF Instantly

Report overview

The global alloy wheels market revolves around the manufacturing and distribution of wheels made from metal alloys, primarily aluminum and magnesium. Alloy wheels are favored over traditional steel wheels due to their lighter weight, superior heat conduction, and aesthetic appeal. These characteristics contribute to improved vehicle performance, fuel efficiency, and enhanced handling. Due to their lightweight nature, alloy wheels are predominantly used in passenger vehicles rather than commercial vehicles, which require higher load-bearing capacity.

Market Size

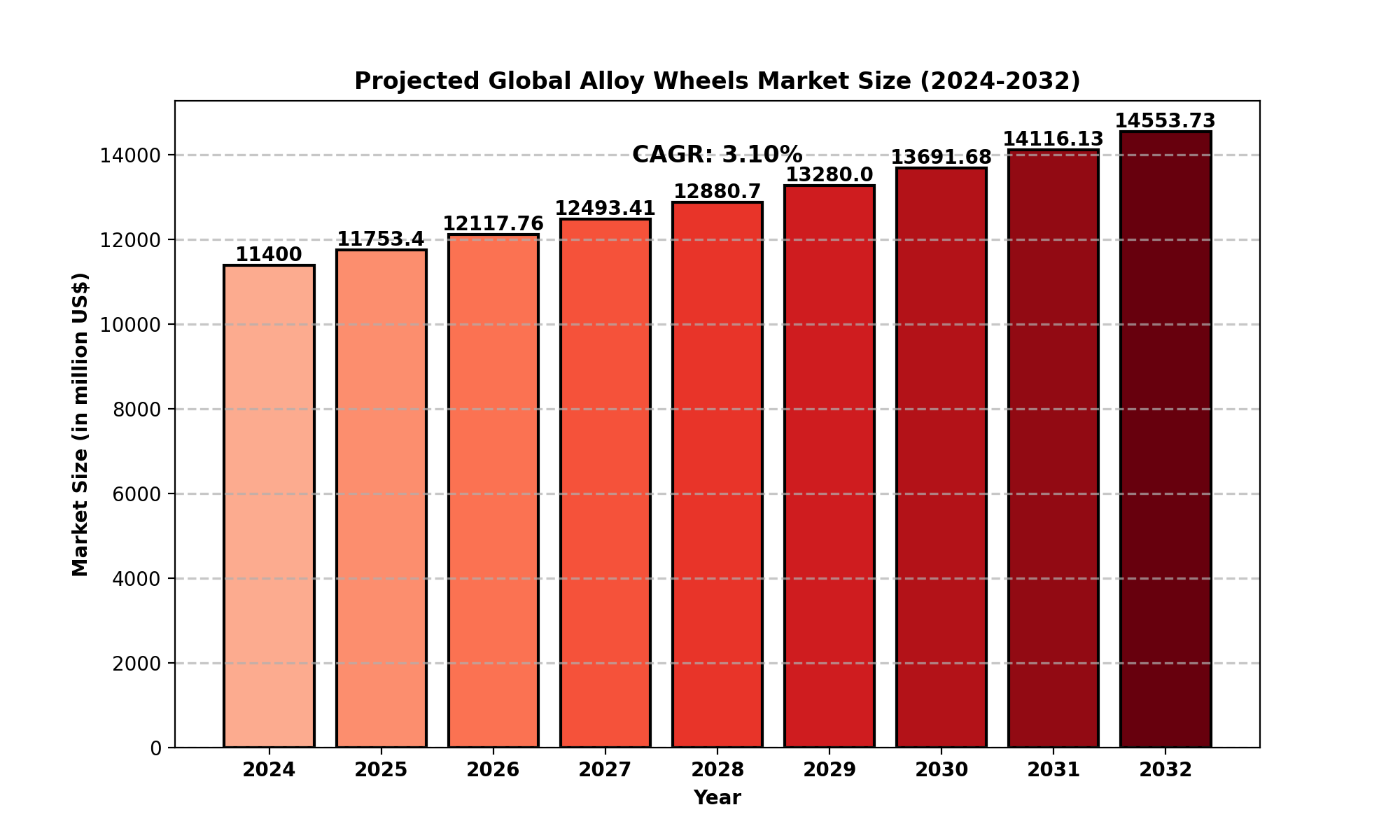

As of 2024, the global alloy wheels market is valued at approximately USD 11.4 billion and is projected to grow to USD 14.55 billion by 2032, reflecting a CAGR of 3.10% during the forecast period.

The North American alloy wheels market alone is valued at USD 3.13 billion in 2024, with an estimated CAGR of 2.66% from 2025 to 2032.

The growing demand for high-performance vehicles, coupled with advancements in wheel manufacturing technologies, is driving market expansion. Additionally, increasing consumer preference for customized wheels and the rising trend of electric vehicles (EVs) are contributing to the steady market growth.

Market Dynamics (Drivers, Restraints, Opportunities, and Challenges)

Drivers

Increased Vehicle Production: The global automobile industry is witnessing a steady rise in production, leading to higher demand for alloy wheels.

Lightweight and Fuel Efficiency Benefits: The lower weight of alloy wheels contributes to improved vehicle performance and fuel efficiency, encouraging automakers to adopt them.

Aesthetic Appeal: The stylish appearance of alloy wheels makes them a preferred choice among car enthusiasts and premium vehicle manufacturers.

Growing Aftermarket Sales: Rising consumer interest in vehicle customization has boosted demand in the replacement and aftermarket segments.

Restraints

Higher Cost Compared to Steel Wheels: Alloy wheels are more expensive to manufacture, making them less accessible for budget-conscious consumers.

Durability Concerns: While alloy wheels offer better performance, they are more prone to cracks and bends under extreme conditions compared to steel wheels.

Opportunities

Rise in Electric Vehicles (EVs): As EVs gain popularity, lightweight materials like alloy wheels are expected to see increased adoption to enhance battery efficiency.

Innovations in Manufacturing Techniques: Advancements in forging and casting technologies are likely to reduce production costs and improve wheel strength.

Challenges

Fluctuating Raw Material Prices: The prices of aluminum and magnesium, key components of alloy wheels, are subject to market fluctuations, impacting profitability.

Environmental Concerns: Manufacturing processes of alloy wheels generate emissions, raising concerns over sustainability.

Regional Analysis

North America

Estimated Market Size in 2024: USD 3.13 billion

Key Drivers: High consumer demand for luxury and performance vehicles, strong aftermarket sales.

Leading Countries: USA, Canada, Mexico.

Europe

Strong presence of premium car manufacturers driving demand for alloy wheels.

Leading Countries: Germany, UK, France, Italy.

Asia-Pacific

Largest regional market, driven by increasing automobile production in China, Japan, and India.

Rapid urbanization and rising disposable income fueling demand.

South America & Middle East/Africa

Emerging markets with moderate growth potential.

Rising automotive investments contributing to market expansion.

Competitor Analysis

Key Companies

CITIC Dicastal

Borbet

Ronal Wheels

Howmet Aerospace

Superior Industries

Iochpe-Maxion

Wanfeng Auto

Lizhong Group

Enkei Wheels

Zhejiang Jinfei

Accuride

Topy Group

Zhongnan Alloy Wheels

YHI International Limited

Yueling Wheels

Market Segmentation (by Type)

Casting: Most commonly used manufacturing process due to cost efficiency.

Forging: Produces stronger and lighter wheels, preferred for high-performance vehicles.

Other: Includes hybrid methods and innovative material combinations.

Market Segmentation (by Application)

Passenger Vehicles: Largest segment, driven by consumer preference for stylish and performance-enhancing wheels.

Commercial Vehicles: Limited adoption due to the higher durability requirements for heavy-duty usage.

Geographic Segmentation

North America: USA, Canada, Mexico.

Europe: Germany, UK, France, Italy, Russia.

Asia-Pacific: China, Japan, South Korea, India, Southeast Asia.

South America: Brazil, Argentina, Colombia.

Middle East & Africa: Saudi Arabia, UAE, South Africa, Nigeria.

Emerging Trends

Adoption in Electric Vehicles (EVs): Lightweight alloy wheels contribute to improved EV range and efficiency.

3D Printing in Wheel Manufacturing: Potential for customized designs and enhanced durability.

Sustainable Production Methods: Increasing focus on environmentally friendly materials and processes.

FAQs

What is the current market size of the alloy wheels industry?

Which are the key companies operating in the alloy wheels market?

What are the key growth drivers in the alloy wheels market?

Which regions dominate the alloy wheels market?

What are the emerging trends in the alloy wheels market?

Key Benefits of This Market Research:

Key Reasons to Buy this Report: