TOP CATEGORY: Chemicals & Materials | Life Sciences | Banking & Finance | ICT Media

Download Report PDF Instantly

Report overview

Medical microfluidic devices are small-scale technologies designed to handle and manipulate fluid samples at microscopic scales. These devices enable the precise control of liquids such as blood, plasma, and other bodily fluids for diagnostic, monitoring, and therapeutic purposes. At the core of these devices is the concept of microfluidics, where fluids are guided through tiny channels or chambers within the device, allowing for quick and efficient analysis with minimal sample volumes.

One of the most prominent applications of medical microfluidic devices is lab-on-a-chip (LOC) technology, which integrates various laboratory functions onto a single chip, typically no larger than a credit card. LOC devices are revolutionizing diagnostics by offering faster, more cost-effective solutions for detecting diseases at an early stage, as well as personalized medicine through point-of-care testing.

In addition to diagnostic applications, these devices are also used in drug development, pharmaceutical research, and therapeutic treatments. Their ability to perform chemical and biological analyses on a small scale makes them indispensable in modern healthcare settings, enabling more accurate results in less time.

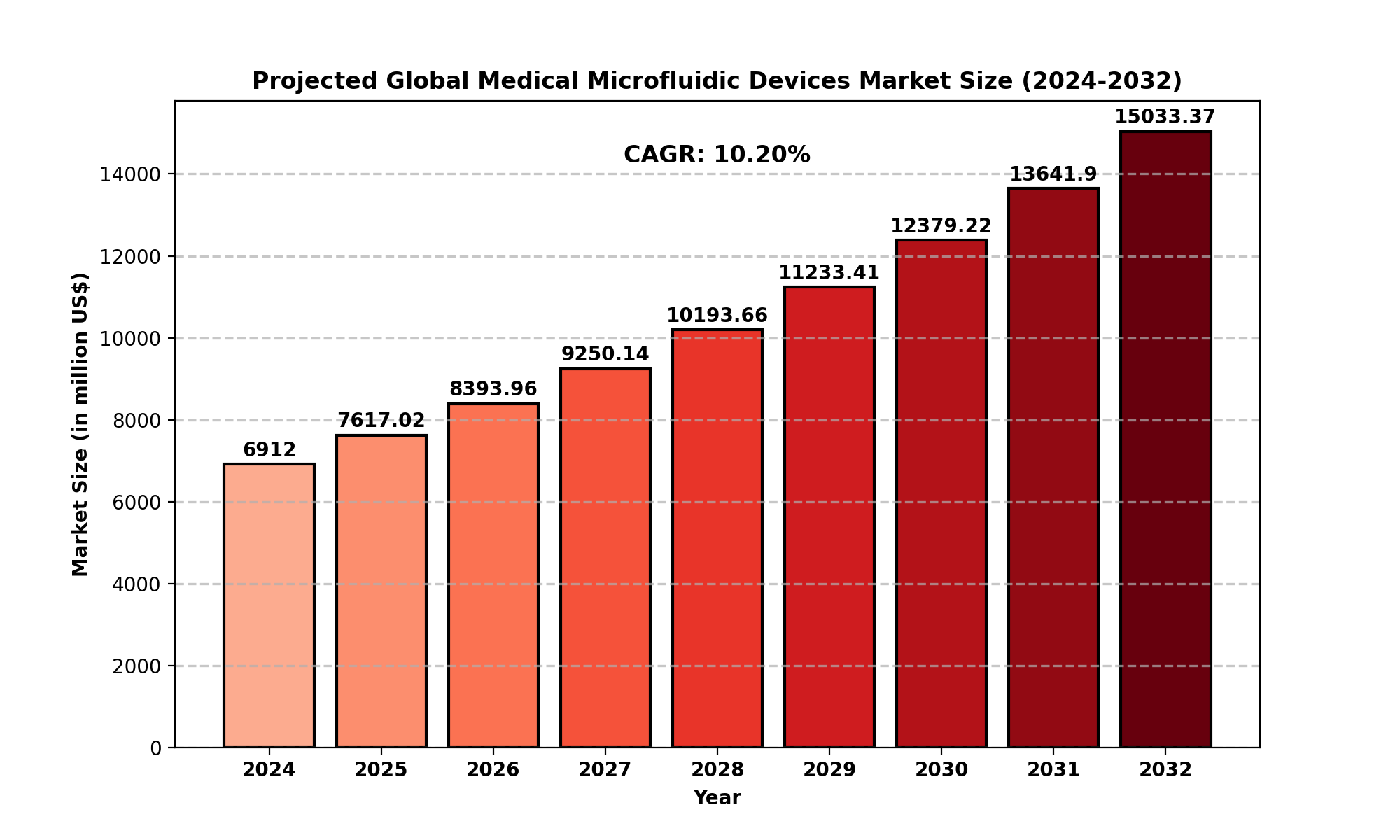

The global medical microfluidic devices market was valued at USD 6,912 million in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 10.20% from 2024 to 2032, reaching an estimated USD 15,033.37 million by the end of the forecast period.

This market growth can be attributed to the increasing demand for point-of-care diagnostics, the rise of personalized medicine, and the growing adoption of lab-on-a-chip devices for drug development and clinical diagnostics. Additionally, the increasing prevalence of chronic diseases such as diabetes, cardiovascular conditions, and cancer has significantly boosted the demand for early disease detection technologies, contributing to market expansion.

Historical Trends:

Over the past decade, microfluidics technology has seen remarkable advancements, driven by the development of new materials, more efficient fabrication techniques, and enhanced device capabilities. Early microfluidic devices were limited in their functionality and scalability, but innovations in design and production have allowed for more diverse applications in healthcare.

Drivers:

Rising Demand for Point-of-Care Diagnostics: The healthcare industry is increasingly shifting toward point-of-care (POC) diagnostics due to the need for rapid, accurate, and affordable medical tests. Microfluidic devices offer the ideal solution for this shift, allowing healthcare professionals to conduct tests outside traditional laboratory settings.

Technological Advancements: Continuous improvements in microfluidics technology, such as enhanced device integration and automation, are making these devices more reliable and capable of performing complex diagnostics. This drives further adoption, particularly in personalized medicine.

Growing Prevalence of Chronic Diseases: The global rise in chronic diseases, including diabetes, cancer, and cardiovascular diseases, has significantly increased the demand for early-stage diagnostic tools. Microfluidic devices help identify these diseases at an earlier, more treatable stage.

Restraints:

High Initial Costs: Despite their many benefits, the initial setup and development costs for medical microfluidic devices can be high. This presents a barrier for small healthcare providers or developing economies to adopt such technologies.

Technical Challenges: The complexity of designing and manufacturing microfluidic devices with high accuracy and precision presents significant hurdles. These technical challenges often delay the commercialization of new innovations.

Opportunities:

Expansion of Emerging Markets: Growing healthcare investments in emerging markets, such as China, India, and Brazil, present opportunities for market players to expand their reach and capture untapped demand for affordable diagnostic solutions.

Integration of Microfluidics in Drug Development: The use of microfluidic devices in drug discovery, development, and testing is expected to see significant growth. Pharmaceutical companies are leveraging these devices for high-throughput screening and real-time testing, accelerating the development of new treatments.

Challenges:

Regulatory Hurdles: Microfluidic devices, particularly those used in medical applications, must comply with stringent regulatory standards, which can be time-consuming and expensive for manufacturers.

Market Competition: The market for medical microfluidics is highly competitive, with numerous players entering the space. This intense competition can lead to pricing pressures and challenges in differentiating products.

North America:

The North American market for medical microfluidic devices was valued at USD 2,129.77 million in 2024 and is expected to experience a growth rate of 8.74% from 2025 to 2032. The U.S. dominates the North American market, owing to its advanced healthcare infrastructure, significant investments in healthcare innovation, and strong presence of leading players like Roche, Abbott, and Siemens Healthcare.

Europe:

Europe is also a key region for the medical microfluidic devices market, with countries like Germany, the U.K., and France leading the way. The adoption of advanced diagnostic solutions in the healthcare systems and the growing demand for personalized medicine are major contributors to the market's growth in this region.

Asia-Pacific:

The Asia-Pacific region, particularly China and India, is anticipated to witness rapid growth in the medical microfluidics market. Increasing healthcare investments, rising healthcare awareness, and the expansion of the middle class are driving demand for cost-effective diagnostic solutions.

South America:

The South American market is expected to grow steadily due to rising healthcare expenditures and the increasing adoption of microfluidic devices in countries like Brazil and Argentina. However, market growth is hindered by economic challenges and lower healthcare spending in certain regions.

Middle East and Africa:

The Middle East and Africa market for medical microfluidic devices is in its early stages, with slow adoption rates. However, the growing healthcare sector, particularly in the UAE and Saudi Arabia, and rising investments in healthcare infrastructure are expected to drive growth in the coming years.

Some of the key players operating in the medical microfluidic devices market include:

Roche: A leader in diagnostics, Roche offers a wide range of microfluidic devices designed for early disease detection and personalized medicine.

Abbott: Known for its innovations in medical diagnostics, Abbott has integrated microfluidic technology into its point-of-care testing solutions.

Fluidigm Corporation: Specializes in providing microfluidic devices for both clinical diagnostics and life sciences applications, including next-generation sequencing.

Johnson & Johnson: A major player in healthcare, Johnson & Johnson has incorporated microfluidic technology into its diagnostic and therapeutic devices.

Siemens Healthcare: Siemens has been at the forefront of integrating microfluidics with advanced healthcare technologies, focusing on in-vitro diagnostics.

Agilent: Agilent's microfluidic devices support applications in life sciences, including clinical diagnostics and pharmaceutical research.

Bio-Rad Laboratories: Known for its innovations in molecular biology, Bio-Rad is expanding its microfluidic technology into clinical diagnostics.

This report provides a deep insight into the global Medical Microfluidic Devices market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and assessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Medical Microfluidic Devices Market. This report introduces in detail the market share, market performance, product situation, operation situation, etc., of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Medical Microfluidic Devices market in any manner.

In-vitro Diagnostics (IVD)

Pharmaceuticals and Medical Devices

Other

Polymer

Glass

Silicon

Other

Roche

Abbott

Fluidigm Corporation

Johnson & Johnson

Siemens Healthcare

Agilent

Bio-Rad Laboratories

North America (USA, Canada, Mexico)

Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

South America (Brazil, Argentina, Columbia, Rest of South America)

The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

What is the current market size of the Medical Microfluidic Devices Market?

Which are the key companies operating in the Medical Microfluidic Devices Market?

What are the key growth drivers in the Medical Microfluidic Devices Market?

Which regions dominate the Medical Microfluidic Devices Market?

What are the emerging trends in the Medical Microfluidic Devices Market?